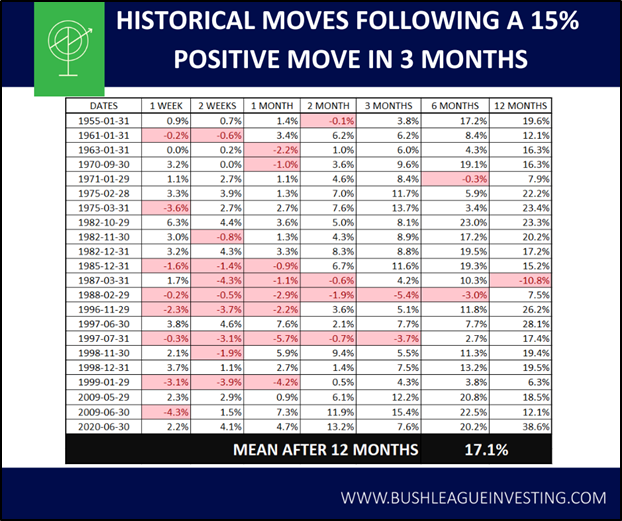

The S&P 500 has been on an absolute tear for the last 3 months. Investors are feeling both extreme FOMO and that we have stretched too far and the market is about to correct. Both interpretations are valid so to stop ourselves from making long-term decisions based on emotion, it is best to look at what has happened in the past after an epic rally like this.

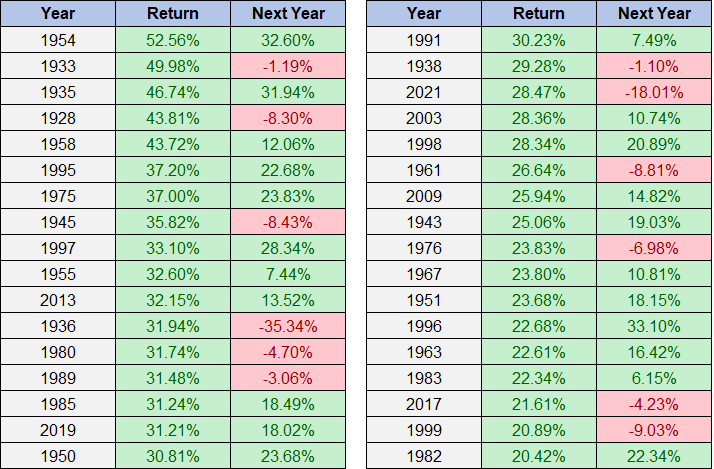

As it turns out, the market has had a run like this 22 times since the 1950’s and 21 times ended up higher 12 months later. This is not surprising as the market normally goes up, but it’s important to note that even after big moves there are always more opportunities. Investors who completely sell off after big moves or who give up thinking they have missed out are destined to watch it keep going higher 95% of the time.

This doesn’t mean it can’t be down 12 months from now, just that the odds favour a continued push up.

I will continue to be invested and wait until the charts, fundamentals or macro screams it is time to get out.

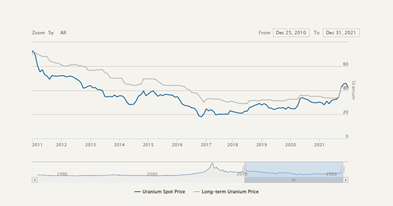

Uranium has been one of my best investments for the last two years. There is still plenty of room to run however it has become frothy as all the pyjama traders and large institutions try to position themselves correctly for the opportunity here. It is possible that “easy” money has been made trading uranium, but this is still a very asymmetric trade in my view. If you are willing to stomach increasing volatility, this may be worth a look.

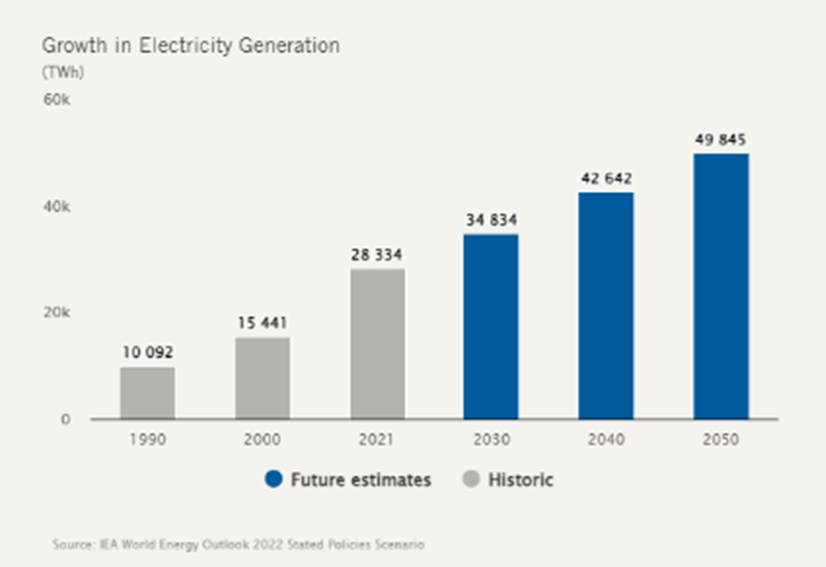

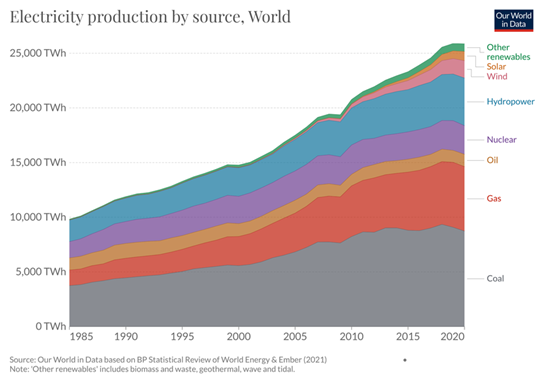

My argument here has only improved in the last 24 months. The world continues to require more energy as a few hundred million more people have started to experience and expect the same quality of life as we have enjoyed in the West. Policy choices around the world regarding fossil fuels and alternative energy use has backed the energy sector into a corner making it increasingly difficult to cover the required demand.

What has changed in the last few months?

Energy sovereignty has become increasingly important across the world. The example I always default to is Germany. I think they will go down as the premier example of of how to get everything wrong for the right reason. 10 years ago, Germany was leading the charge to use alternative energy and they started decommissioning everything that was considered ‘not green’. This was being done to meet environmental goals and was shown as a template for others to follow. Currently, they are burning record amounts of coal, their production based economy is in ruins due to high energy prices, and the amount of weekly power they can use for industry has a cap so their citizens don’t freeze to death. This is the result of producing much less power with contingency plans to buy energy from Russia to offset the unreliable alternative energy production. Germany is the best example, but many major countries are looking at their current and future energy needs and have seen the importance of energy sovereignty.

After 3 decades of condemning nuclear power, Germany, Canada and many other players have decided nuclear is clean again. The interesting news out of COP28 is that there is a multi-country declaration to triple world nuclear capacity by 2050. Currently, China has 25 reactors under construction with 200 in the planning phase. France, who has benefited greatly from keeping their reactor fleet operational, has plans to build out in the near future.

SMR, “small modular reactors”, are the new game in town. Much quicker to build, lower initial cost and proximity to urban centers are some of the benefits of this type of reactor.

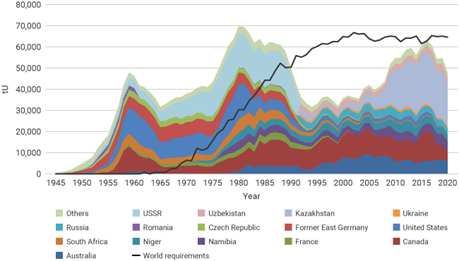

Maybe the biggest driver of the recent spike is that Kazatomprom (Kazakhstan’s national operator for uranium mining) has released that they will not hit their production guidelines. They are far and away the largest supplier of uranium to the market.

So what do we do with this information? (This is not financial advice; please do your own research).

I am holding. I think there will be some wild swings in the next 24 months. When it spikes, I will trim 10-25% off, and when it dips, I will be a buyer until any of the drivers of this story change. The chart looks like it is about to moon, but this story is very popular right now and any news will hit harder than it has over the last few years.

Some other thoughts:

Uranium is almost profitable to mine at current prices

At current production levels, more is being consumed than created yearly and a uranium mine takes years to begin operations. No large mines are currently slated for the next five years.

The price of uranium is almost inconsequential to the cost of running these facilities so the utilities will buy it even if it is 10x the cost it is now (not a prediction).

If you’re interested in diving deeper, the Uranium Insider puts out daily info specific to uranium. He has a newsletter and does YouTube videos.

It is the start of another year and the investing world is struggling to find a narrative for 2024. For the 15th year in a row, the usual doom and gloom crowd is predicting that the financial system will collapse and the super optimistic few think this is the beginning of another super cycle with resonance to 1994. As in most things, the answer will most likely fall in the middle and will follow historical precedence.

To avoid falling into the emotional traps of fear or greed, a good place to start is looking at what has happened before.

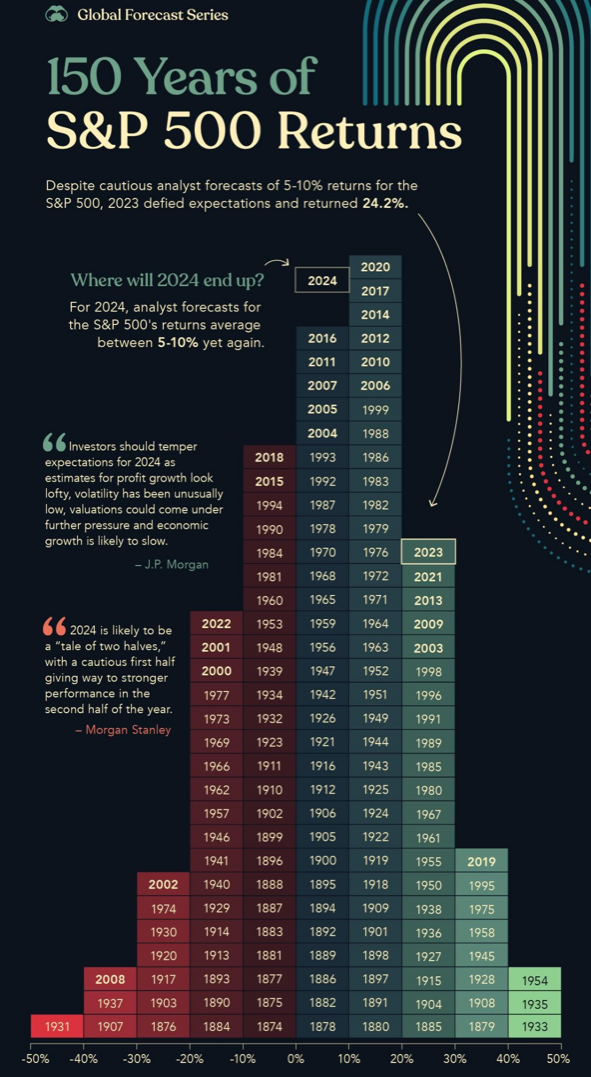

On average, the S&P 500 goes up approximately 9% a year so at the beginning of every year this is where I set my expectation. I balance my expectations by staying on top of current market developments but also through research and analysis of historical data points and patterns. For example, if we ask what to expect from the market after being up 20% (2023 was up 24%) an historical lens will show us that since 1928 the market has been up 22 out of 34 times the year after a 20%+ year. Some other data points leaning in favour of an upcoming green year is that the 4th year in a presidential cycle is positive 75% of the time, and in cycles with a red mid term year, the market has been green 100% of the time. This info isn’t predictive but shows what has happened in similar situations in the past (source).

These data points are helpful for perspective and to remain grounded; they are certainly not screaming sell everything and hide your money under your bed.

With the context of past market behaviour, there are enough reasons to be both optimistic and cautious in 2024. I tend to highlight positive reasons and data here because negativity normally gets the airtime. 2024 is a hard year for market predictions but, luckily, no one needs to predict anything If we trade and invest in what we see and not what we hope or fear we will see, we will be much less likely to make an emotional trade we regret. I will continue to own shares in companies I believe are great and hold them until I have a reason not to. If the market starts telling us that it is headed down in a big way, I will sell 25-50% of my shares in these companies and wait until I can see a game on sign in the charts and earnings to jump back in.

The entire premise of this website is to demonstrate that amateur investors can generate higher returns than simply buying the S&P 500, or worse, paying someone else to buy it on their behalf. The slightest outperformance over the market each year can add up to huge amounts over an investing lifetime and the best part is that anyone can do this with a bit of patience and time spent looking into companies and how markets and money work. You can make it as simple or as difficult as you want. I have been doing this “seriously” since January 2014 and have been rewarded so far for the patience and effort.

Close to 500% in 10 years, more than double the S&P 500!!!

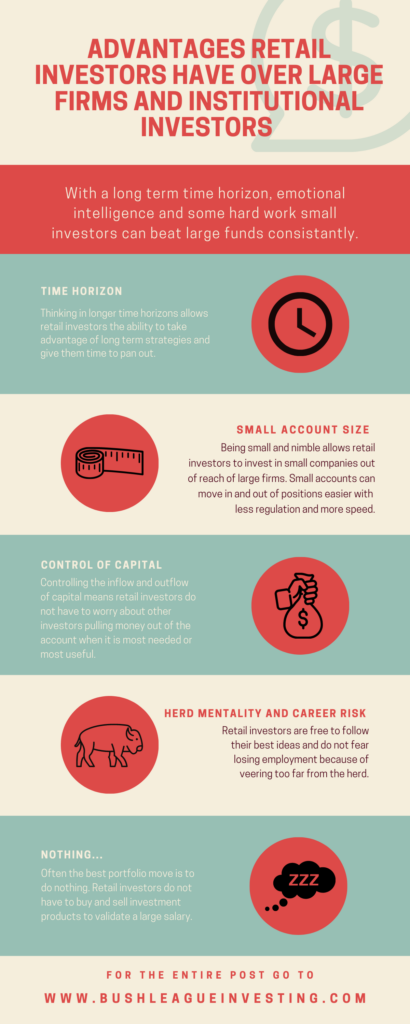

The very first post on this website was an attempt to outline the advantages retail/amateur/small dumb money investors have over the big players. I think they all still hold up. I would emphasize again that large funds are unable to change directions quickly where retail traders have the advantage of being much more nimble.

Think of positions that big players hold like huge cruise ships or oil tankers. At sea, those huge ships must make their directional choices far from when they are needed. From top speed it can take almost a kilometre to stop some large tankers. Smaller traders can react more like a jet ski in comparison. This can lead to over trading, but there is peace of mind knowing your entire portfolio could be sold for cash within a few seconds.

Follow the portfolio to get a monthly update on how it is doing.

The market is currently frustrating both bulls and bears as we sit on a major resistance level that both sides are convinced we are about to break out from. I don’t really have a directional view in the near term, but am watching this level intently as it should be a violent move either way.

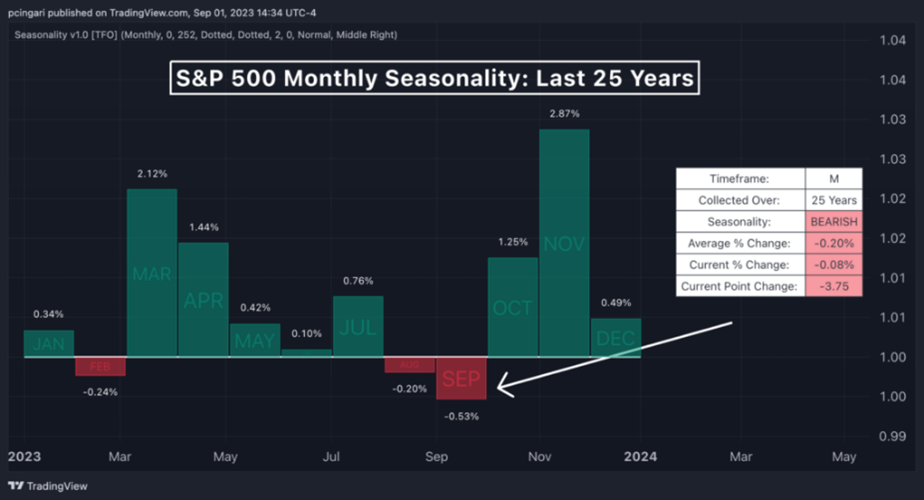

There are enough people pushing doom and gloom, so I don’t feel like I need to go into the negative case for a downturn. On the positive side, one of the more interesting arguments is a seasonal one. The market historically follows a few patterns one of which is that the 4th quarter is normally positive and usually the most positive. August and September are historically rough and October is known as the bear killer. I have seen a few “Uptober” posts already. We will have to see how this plays out, but it should be a big jump in either direction from here.

Follow the portfolio to see our reaction to how this directionally important crossroads unfolds.

Uranium has had a great run in the last two years. If you have been following the portfolio, you have seen it become a larger and larger percent of the holdings. I sold 1/3 of the position this past month because the move was a bit too extended. I thought this would be a good a chance to offer my two cents on uranium and explain how I trade around long-term positions in the portfolio.

I started building a position in February 2021 and it has been a great climb since. I use the Sprott Physical Uranium Trust to participate in moves in uranium. So far we are up around 140% on the position.

I use macro ideas to get into positions but then I use some technical analysis to tell me if I should add or trim. I sold mid month because the move was very quick and the price was reaching the top of the channel I was watching.

When positions become too stretched, I like to take some out, usually 30%. My intention is never to time anything perfectly but adding during weakness and trimming into strength has served me well if the reasons I started the positions are still valid.

Uranium continues to be one of my highest conviction positions going forward. I am expecting a 15-20% correction and then another big move up over the next 12-18 months. I have laid out my thesis multiple times and it seems to only be improving. Click here to read what I previously said about uranium.

With so much going on in the economy and the markets right now, my preferred investment strategy is to focus on a few ideas with high conviction rather than spreading my attention too thin with a broader approach. A high conviction idea to me is an idea I am willing to commit more time to researching and more capital to in the portfolio.

Going forward this year my two highest conviction investments are uranium and natural gas. It is incredibly hard to time anything in the markets and at the top of the list of difficulty is commodities. They are often counter trend plays that can sometimes lag the economy or precede big moves of the S&P 500.

A lesson I have learned from over a decade in the market is investing is never a sure bet; the best you can do is stack the odds as far in your favour as possible and wait for signs that you are correct.

Uranium

This has been on our radar for over a year now and it seems to be finally looking ready to blast off. We started a position in Feb 2021 and so far it is up 80.23%. In our view however this could just be the pregame stretch.

Why?

The world needs more power and there are a few billion people who want a quality of life closer to that which is experienced in wealthy countries. This requires energy; people are not likely to agree to live in a situation where their options are limited because it isn’t windy, or it has been cloudy for a few days.

This increase in demand combined with the unintended consequences of ESG policy over the last 10 years has created a record amount of coal being used in places like Germany and California. Nuclear is the cleanest and most dense source of energy available and compared to the rising use of coal, it seems like a no-brainer. Reactors have started to make a comeback in Asia and the Middle East with China currently leading this adoption with 19 reactors under construction.

Uranium has been trading below the cost to produce it for years and the over supply is eroding. There are now physical trusts (U.UN) that are scooping pounds off the market and the energy companies are competing for pounds more than in recent history. When the supply glut runs out, this could be a huge move! Even if the price of uranium were to increase 10x from here, it is still such a small price compared to the billions to bring the reactors online that it almost doesn’t matter.

The investment I am using to try to benefit from this idea is U.UN.

Natural Gas

Natural gas requires a huge warning when discussing; people who trade commodities call it the widow-maker because of the huge counter intuitive moves it can make. The upside for this idea is seated in the energy argument along with a few others.

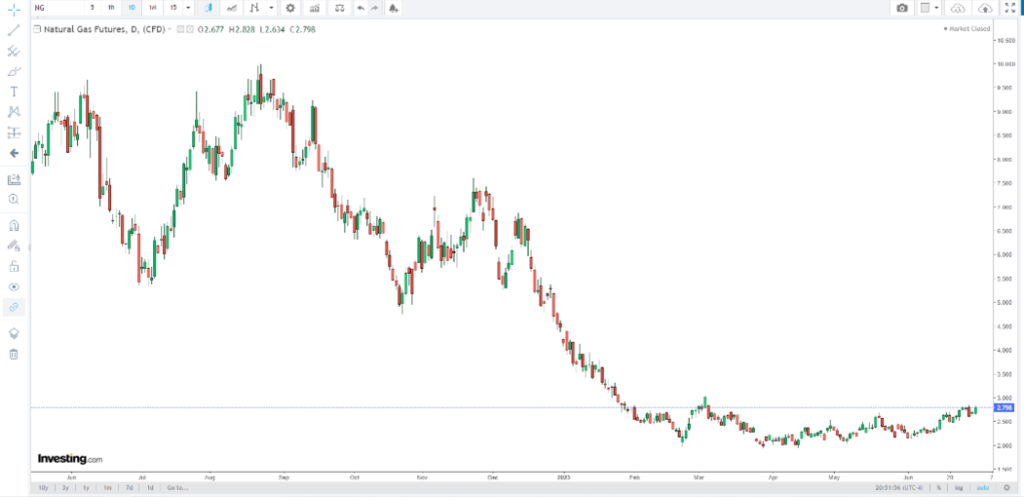

There is a huge spread between natural gas in the EU (10.11) and in the US (2.77) and as these two partitioned gas “economies” connect the price will move in theory to land somewhere in the middle. There is seasonality at play here too that helps as historically the price rises in the fall.

How am I wrong?

Uranium: If energy demand doesn’t continue to rise, this thesis will not play out. If there is another unfortunate event at a newish reactor, demand will fall off a cliff for safety reasons.

Natural Gas: If it acts like natural gas and defies reason, this might not win. Careful.

Good luck trading! (These are not recommendations. Look into these two ideas yourself! This is just what I am doing.)

Fossil fuels touch almost every part of our lives from energy production, as an input of a product, and a primary means through which everything is transported. Cosmetics, plastics, fertilizers, fuel, cleaning products and clothing represent only a few of the goods made directly with oil. In the last 150 years peteroleum products have revolutionized how almost everything is done resulting in an ever increasing need for oil.

Currently in Canada we consume approximately 1047 gallons per person per year. Many other large nations, India and China for example, remain far behind this number but are catching up quickly. These two countries at 51.4 gallons and 137.8 gallons respectively will only continue to increase their consumption as their GDP continues to rise and their citizens begin to enjoy a higher quality of life.

Energy is essential for growth and prosperity, but it comes at a steep price paid by the environment and our public health. These issues need to be addressed but unfortunately it is not reasonable to turn off oil before there is something viable to replace it. Currently many countries that have jettisoned fossil fuel sovereignty for dreams of becoming greener are paying for that choice. Germany is at the forefront of this energy crisis having shut down nuclear plants in favour of relying heavily on solar and wind power. Ironically unless they abandon plans to close their reactors down, they will be burning coal for the next two years to offset their energy woes. This story is ripping through Europe with France as the exception.

Why is there a problem?

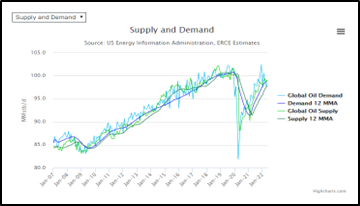

We have under invested in energy creation in the last ten years. It has been seen as undersirable and harmful to have E & P companies on the investment sheets of funds and ETFs not only due to its bad reputation but also because the cost of capital has been much higher for companies because of ESG regulations. This is simple supply and demand; demand will continue to grow and supply is far behind and slow to adjust.

It can’t go higher because it will break everything!

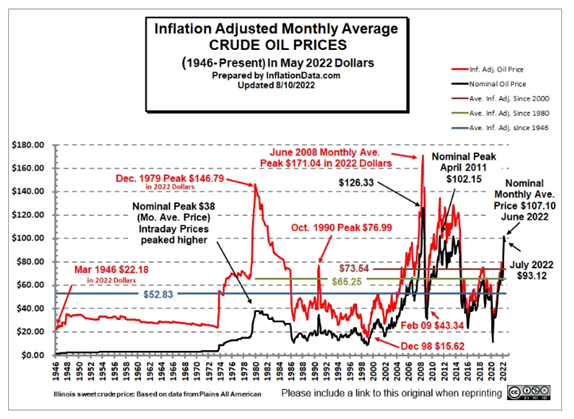

Currently oil is high but if adjusted for inflation, it doesn’t seem so extreme. It is hard to not just see the pump price and compare to past prices, but what doesn’t usually factor in people’s thinking is what the purchasing power of their dollars was when oil/gas was lower. Even near $100/barrel, we are not that close to “all time highs”; oil can go much higher before anything breaks.

How am I wrong?

Knowing what will destroy your thesis is crucial to not blowing up your trading account. One way my forecast will be incorrect is if there is a large and long recession in the US and Canada. A short-lived recession will not be enough to destroy demand to a level where there is extra supply. Even emptying the SPR (Strategic Petroleum Reserve) to its lowest level in 30+ years could not stabilize supply and demand.

Prediction:

WTI will be $125 by Christmas and $150 by March 2023.

Oil companies, leaps on oil ETF and the same for uranium is how I am playing this.

After my worst year in the books (+9.2%) since 2014 (+5.25%), it’s time to regroup and plan for the upcoming year. Although 9.2% is positive, with inflation CPI at 7% and the S&P 500 up 28.7%, it’s hard not to be a bit disappointed. Here is a quick summary of last year followed by a rough framework that I will be using for 2022.

What worked in 2021:

RIOT and HIVE screamed out of the gate early in the year only to trend lower with a bit of a bump in the fall then continued to lose value for the rest of the year

BRK.b (Berkshire Hathaway) was quietly up 30% and is a position that I don’t need to worry or think about for many years

UCO/U.UN have both increased around 30% since I added them to the portfolio and I will discuss my thoughts on oil and uranium in this year’s plan

VCI (Vitreous Glass) continues to be my largest position and like clockwork continues to pay a huge dividend under the radar while also increasing in value

What didn’t work in 2021:

NUGT and SILJ: These two leveraged ETFs both finished down for the year. I expected these to do much better than they did, but I came out about even because of selling at highs and buying at lows. Holding leveraged ETFs is a risky move; they can really turn against you quickly and the expenses require a good move up to break even.

Hedges: I used hedges such as UXVY, FNGD and SPXS throughout the year. Hedging is a large part of my overall strategy, but with limited market access for large periods of time this year hedging cost a lot (approx. 12% of overall performance in 2021) with minimal benefit. If there had been a violent drawdown, I would be listing this in the ‘what worked’ section.

Looking forward to 2022

Already it’s a very different market in 2022. Talks of rate hikes and quantitative tightening have people thinking less optimistically and the same people who have called for the end of the financial system since 2002 are back at it and gaining a larger audience.

I wrote about inflation back in June and January of last year and that is still an important part of the puzzle for 2022. My thoughts haven’t changed on how to do well during periods of high inflation and I will continue to hold my gold, silver and crypto stocks.

My new additions to this strategy are oil and uranium. In the last few months these have done very well and the best part is I think they are just getting started.

2022 Ideas

OIL

While I agree with the move to green energy being best for the planet and essential for our long-term survival, to be successful the switch has to happen in a logical and gradual way. For the last 5 years, fossil fuel companies have been treated like tobacco companies with lending for oil exploration being non-existent and higher rates imposed on companies in the sector because they are not in line with ESG (Environmental, Social, and Governance) criteria. There are some interesting results of policies punishing carbon-based fuel that will make for potential returns.

As more of the world increases production and consumption closer to North American and European levels, energy requirements will continue to increase. If supply can’t match this growing demand then the outcome is higher prices and shortages. The shocking part of this is that carbon based energy like coal, oil, and natural gas continue to grow despite other cleaner forms of energy being added. The demand is much greater than the offset of the renewables. A surprising instance of this is in California where almost 50% of electricity is currently produced using natural gas. This means that 1/2 of all Teslas driving around California are powered by natural gas.

In summary:

reduced investment in production

increase in demand

geopolitical tensions growing

URANIUM

This might be my strongest conviction bet for the year. Playing off all the points from oil regarding energy use and need, uranium is in a unique situation. After the devastating disaster in Fukushima in 2011 many countries have slowly separated themselves from their nuclear programs. This has placed uranium in an awful position and the price has declined for the last decade because demand was lighter than supply. Currently the price of uranium is less than the cost to produce it.

With next year poised to require much more energy than is currently available, it is my base case that nuclear will be part of the solution. Asia is leading the way with 55 reactors being constructed in mostly China, Russia and India in attempt to generate enough power and retire their mostly coal based power plants. I believe Europe and North America will follow if emission targets are to be met.

However, Uranium mines take a long time to come online. While it isn’t a rare metal, being able to extract it and supply it in its usable form is difficult. Three countries supply most of the world’s uranium (Kazakhstan 41%, Australia 13%, Canada 8%) and recent political unrest in Kazakhstan has energy producers concerned regarding future deliveries.

In summary:

energy requirement is not currently possible

uranium still isn’t worth the cost of mining it

industry slow to turn on supply when it becomes profitable

To test and trade these ideas I am using U.UN (Sprott Physical Uranium Trust) and UCO. These are not perfect instruments but will directionally follow the price of the commodities.

VOLATILITY

There are too many reasons to list why this year will be volatile. My plan is to continue to hold a position that increases with volatility primarily through UVXY to benefit from instability. When/if the position reaches 15%, I will sell 5% and pour it back into positions I have high conviction in. I will rinse and repeat for all of 2022. If this doesn’t hit 15%, it will cause 2022 to underperform again; if it hits, this will juice returns.

I hope this summary and plan helps! Please read through the disclaimer on the site. This is my plan and may not make sense for others.

There are many ways to decide whether or not your investments are doing well. The goal most people are shooting for is a decent return without taking on unnecessary risk. With this in mind, you can measure your return against almost anything understanding that a good return and unnecessary risk mean different things to different investors.

Since I have a long-term investing horizon and am comfortable with what I consider medium risk, the S&P 500 is a great benchmark for me to measure my return against. Supposing I was unable to beat this benchmark, it would be super easy to just buy an ETF that tracks the S&P 500 and save myself a massive amount of time and energy. This is what I think is best for people with no time or interest to self-manage their investing. But for those of you with time to dedicate to managing your own portfolios, I encourage you to consider the S&P 500 as a key measuring stick to track the growth of your own return.

What is the S&P 500?

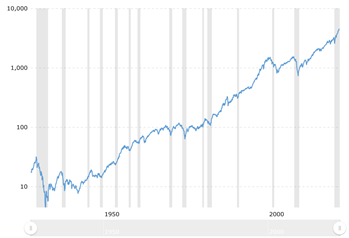

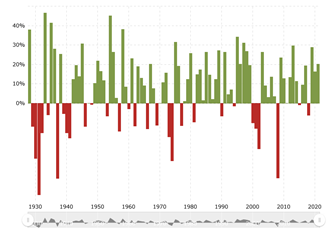

The S&P 500 is a market cap weighted index featuring the 500 largest companies that meet all of the inclusion criteria. The number of holdings changes when current companies issue multiple share classes or there are companies excluded/included to the index. It has returned approx. 10% annually and much higher in the last 10 years. Looking at the below charts showing the index’s history since 1930 it’s hard to imagine losing money just buying this index, but there have been a few rough patches with multi-year losing streaks.

Source: Macrotrends.net

Can you beat it?

Yes

Should you try?

Maybe (if you’re willing to put in the work)

Have I been beating it?

I thought you’d never ask.

Since 2014, the investing account shown below (LIRA – Locked In Retirement Account, Canada) is up 470% compared to the 185% of the S&P 500. I am unable to add or withdraw money from the LIRA, so it’s an accurate view of my actual investing results to date. For the first few years we were beating it, but it was close. Last year, we destroyed the S&P 500. So far this year, I started out ahead and over the last few months the S&P has outpaced me.

Will we always beat the S&P 500?

As recent months have shown, there will be stretches where the index outperforms Bush League; however, I am confident that over any multi-year period the correct move for me will be to continue to manage my own investing.

The case for managing your own investments

I like the ability to profit when the market goes down (it does sometimes), and I like the ability to allocate more capital to ideas I think will do better than the average or that I personally think benefit society. The S&P 500 is market cap weighted which means bigger companies have a bigger effect on the direction it moves leading to a small handful that steer the index (ie. FAANG+M). The perception of owning an index of 500 companies is that there is good diversification, but in my opinion there is much less than most people realize. The below image shows that when big tech has a rough day, the entire index follows.

Heatmap S&P 500 image from finwiz.com

So why compare?

Constantly keeping score against this index allows me to see what is working and what is not in my own portfolio. The S&P 500 is known as the “market”; if people say “the market” is up or down, they are usually referring to this index. If the market has been ripping for years and you are not making any money, comparing your results allows you to evaluate whether you are seeing things as they are or as you think they should be. If I had been stuck watching P/E ratios and complaining that everything was overvalued for the last 7 years, I would have missed what was happening in the market.

My assessment is that my portfolio will continue over long periods of time to beat the S&P 500. When it goes up my portfolio seems to do well and when it crashes, we are hedged so we stand to do very well. In the event I find the way I invest isn’t working compared to the S&P 500 then I will either adjust or buy the index and get a different hobby.

How does your portfolio’s results compare to the S&P 500?

We use cookies to ensure that we give you the best experience on our website. If you continue to use this site we will assume that you are happy with it.Ok